This article was first published in the Financial Mail on 18 March 2021.

Ethical or responsible investing is often considered to have emerged from the 1980s campaigns for divestment from corporations operating in apartheid SA. However, the concept has much older, and strongly religious, origins.

In biblical times, the Jewish concept of tzedek (justice and equity) — applicable to all aspects of life, including the economy — was aimed at correcting the disruption that humans cause to the natural world. Ownership brought with it both rights and responsibilities, and these responsibilities included the prevention of immediate and potential harm.

Sharia law, emanating from the religious teachings of Islam, has evolved to prohibit investment in industries whose primary business is not consistent with Sharia principles.

And, in the 18th century, Methodists in the US resisted investments in the slave trade, liquor, tobacco and gambling, and the Quakers later prohibited investments in slavery and war.

In recent decades, responsible investing, implemented primarily via the integration of environmental, social and governance (ESG) factors into investment decision-making, has grown in importance. It has done so in line with our deepening understanding that the existential threats now facing humanity are the culmination of centuries of ignoring the social and environmental impacts of economic growth.

ESG integration first requires in-depth analysis of the environmental, social and governance risks and opportunities posed by a company’s operations. The extent and nature of these risks and opportunities are then integrated into assessments of future financial performance. The risks assessed are those to the company itself, and the risks its operations pose to society more broadly (for example, the carbon emissions of fossil fuel companies).

In the context of rapidly accelerating climate impacts, biodiversity loss and a world turned upside down by Covid, we have moved quickly from ESG-related issues being considered niche, to an explosion of ESG-and sustainability-related developments across the globe.

Assets under management in sustainable investments (or, at least, in investments labelled “sustainable”), hit a record $1.7-trillion in 2020.

Recently established networks, partnerships and standard-setting initiatives that aim to tackle the negative impacts of global capitalism include the Task Force on Climate-Related Financial Disclosures (TCFD), the Climate Action 100+ investor initiative, the UN Environment Programme’s Principles for Responsible Banking, the Natural Capital Investment Alliance and the Partnership for Carbon Accounting Financials.

Inevitably, however, these developments have been matched by equivalent developments in the scope and sophistication of “greenwashing”.

This makes it increasingly hard for asset owners, pension fund contributors and retail investors to know which companies and financial institutions are really trying to have a positive impact, and which are simply mandating PR agencies and teams to make it look as if they are, while continuing with business as usual.

The phenomenon was captured well by Niall O’Sullivan, chief investment officer for Europe, the Middle East and Africa at global asset manager Mercer, when he commented in a recent blog post: “I have watched with interest over the last number of months as firms that until recently could not spell out ESG, or only came across sustainability when moving between stocks and treasuries in the dictionary, have been trumpeting their developments.”

There has also been a marked increase in this “trumpeting” in the local market.

It is impossible to avoid the adverts, advertorials, blogs, sponsored op-eds, LinkedIn videos, webinar promotions and product offerings of financial institutions, companies, law firms and consultancies claiming to care deeply about sustainability, and touting the expertise of their employees on everything from climate change, pollution and water scarcity, to pay gaps and racial and gender discrimination.

Some of these claims are genuine, as is clear from action that has resulted in real-world impacts. But many are simply a veneer of glossy marketing layered over an unchanged business model.

It is often difficult for customers to know the difference.

Underpinning the challenge is that ESG-and sustainability-related claims and credentials are largely unregulated. All of the initiatives mentioned above are voluntary (though some jurisdictions have started to mandate disclosures aligned with the recommendations of the TCFD), and the mechanisms for ensuring adherence to their principles and recommended practices are weak.

Recent studies have shown how membership of responsible investing initiatives can actually serve as a front for inaction. For example, analysis of a decade of shareholder voting data, by Robeco and the Erasmus School of Economics, found that asset managers predominantly vote against social and environmental shareholder resolutions, and that signatories to the UN-backed Principles for Responsible Investment (PRI) do not vote more often in favour of these proposals. This is despite the fact that these signatories have explicitly pledged to incorporate ESG factors into their investment decision-making.

In an attempt to tackle greenwashing in the financial sector, the EU has developed a sustainable finance disclosure regulation (SFDR), which came into effect on March 10.

The SFDR aims to make the sustainability profile of financial institutions such as banks, pension funds, asset managers and insurance companies measurable, comparable and easier for investors to understand.

The EU rules will have some effect on local listed companies with Europe-based shareholders, but it is unlikely that we will see any robust regulation of this sort in SA for a long time. The private sector prefers “self-regulation”, and the JSE and the Financial Sector Conduct Authority are remarkably poor at enforcing even the weak ESG-related rules SA has.

The ability to analyse ESG risks, to engage meaningfully with company management in relation to these risks, and then to integrate them into investment decision-making, requires an understanding of financial markets, as well as knowledge and expertise in a wide range of nonfinancial subjects.

But there is no formal “ESG analyst” qualification, and responsible investment is not currently integrated into the coursework of finance and business degrees.

While ESG generalists have an important role to play, there is an increasing need for technical specialists, in areas such as climate change, if ESG integration is to result in meaningful positive change.

Effective ESG analysis and engagement requires the ability to critically assess all company reporting, not just financial reporting; a willingness to challenge decision-makers, even when this might affect profitability in the short term; and a world view that appreciates and understands our social and environmental challenges.

This is a difficult role that’s not traditionally associated with the competences of finance professionals.

However, in many financial institutions, ESG-related roles are assigned to people with little power in the organisation to challenge decision-makers.

The absence of any standard measure of ESG competence also means anyone can claim to be an ESG expert without fear of challenge. One SA asset manager, for example, declares in its PRI transparency report (only parts of which are publicly available), to have 69 “dedicated responsible investment staff”.

UK-based shareholder activism organisation ShareAction recently released a guide to leading responsible investment practices for asset managers, covering responsible investment governance, climate change, biodiversity and human and labour rights.

Best practices for responsible investment governance include: mandatory ESG-related training; publicly available voting policies; making voting decisions and rationales available online as soon as possible after AGMs; pre-declaring voting intentions for key ESG-related shareholder resolutions; public reporting on ESG investee engagement, including real-world outcomes that result from that engagement; and a publicly available escalation strategy that outlines steps taken when engagement is unsuccessful.

SA asset managers’ implementation of these governance best practices is patchy, and public escalation strategies almost nonexistent. When it comes to best practice on climate change, biodiversity and human rights — think fossil fuel exclusion policies, portfolio decarbonisation commitments and portfolio targets on biodiversity-related topics — we see very little at all.

Because most ESG-related engagement by asset managers happens behind closed doors, with little demonstrable link to real-world outcomes, the best way to cut through the ESG data dump in annual reports is to go straight to remuneration policies. This shows very clearly that only a handful of JSE-listed companies take ESG seriously enough to integrate responsible investment objectives into remuneration.

In the few cases where there is a link, ESG metrics influence about 10% of short-term incentive awards. Even where short-term bonuses and long-term incentives are tied to an ESG objective, these are almost always because that objective relates to a pre-existing legal obligation, such as health and safety.

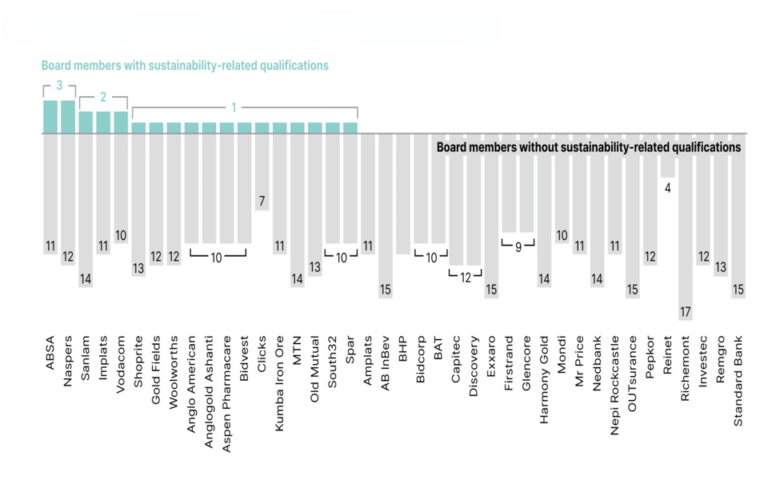

Another clue is the ESG competencies of corporate boards. The director of the New York University Stern Center for Sustainable Business highlighted recently in the Harvard Business Review the extent to which “boards remain a stubborn outlier when it comes to embracing sustainability”, and that much of the problem lies in a lack of expertise.

For example, of 1,188 Fortune 100 board members assessed, only five had relevant expertise in climate and water — issues of material importance to most companies and investors.

While ESG analysis provides insights into material issues that have traditionally been neglected in investment decision-making, the financial sector too often forgets that the underlying purpose of all these efforts is to create a world where our development does not destroy the natural systems we rely on to thrive.

Sustainable development, originally defined in the World Commission on Environment & Development’s 1987 “Brundtland Report”, is “development that meets the needs of the present without compromising the ability of future generations to meet their own needs”.

We have reached a number of tipping points on climate, biodiversity and inequality: our inadequate action to date means that the window of time we have to change is narrowing, and our options are becoming increasingly constrained.

Greenwashing is not just an undesirable business practice: if left unchallenged, it threatens our ability to tackle the great crises of our time.